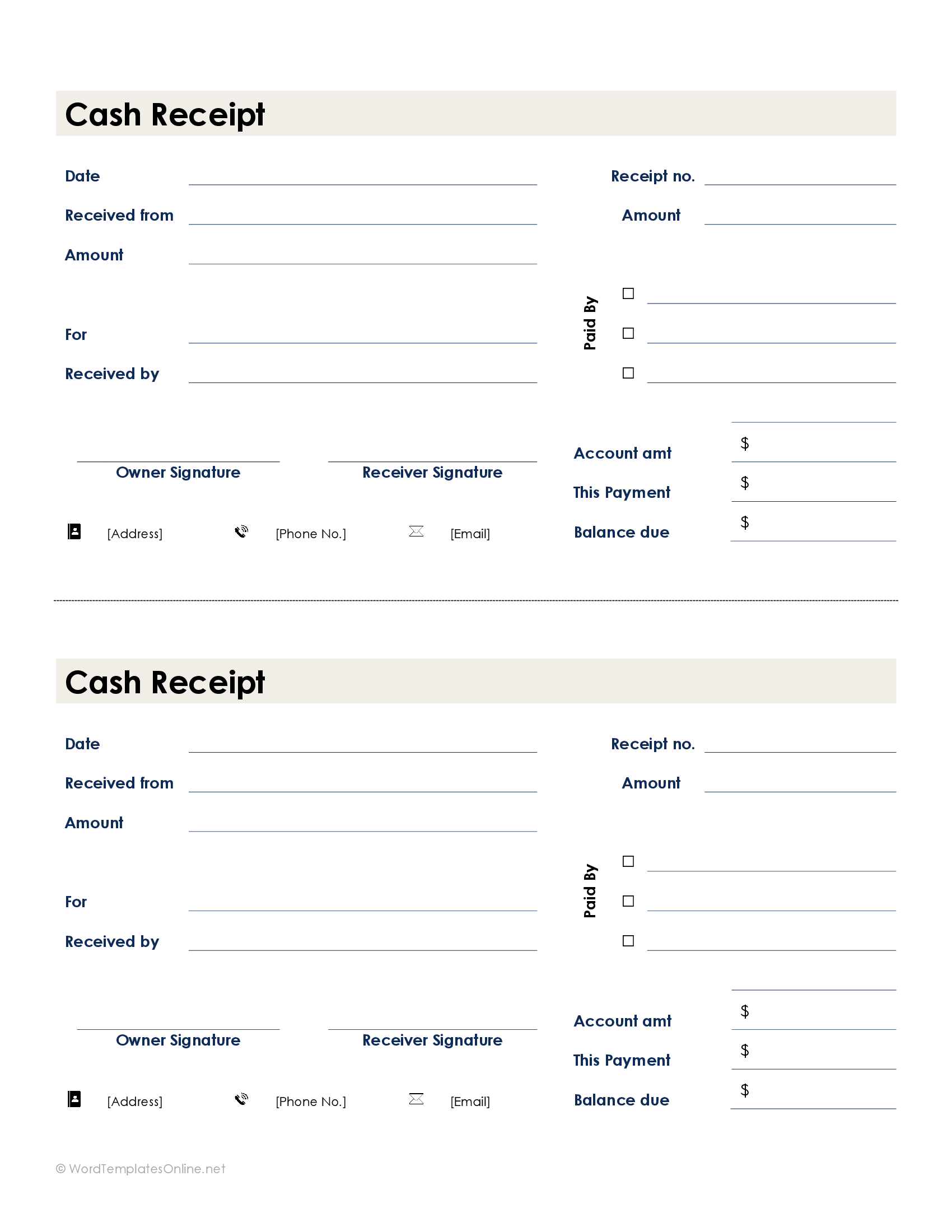

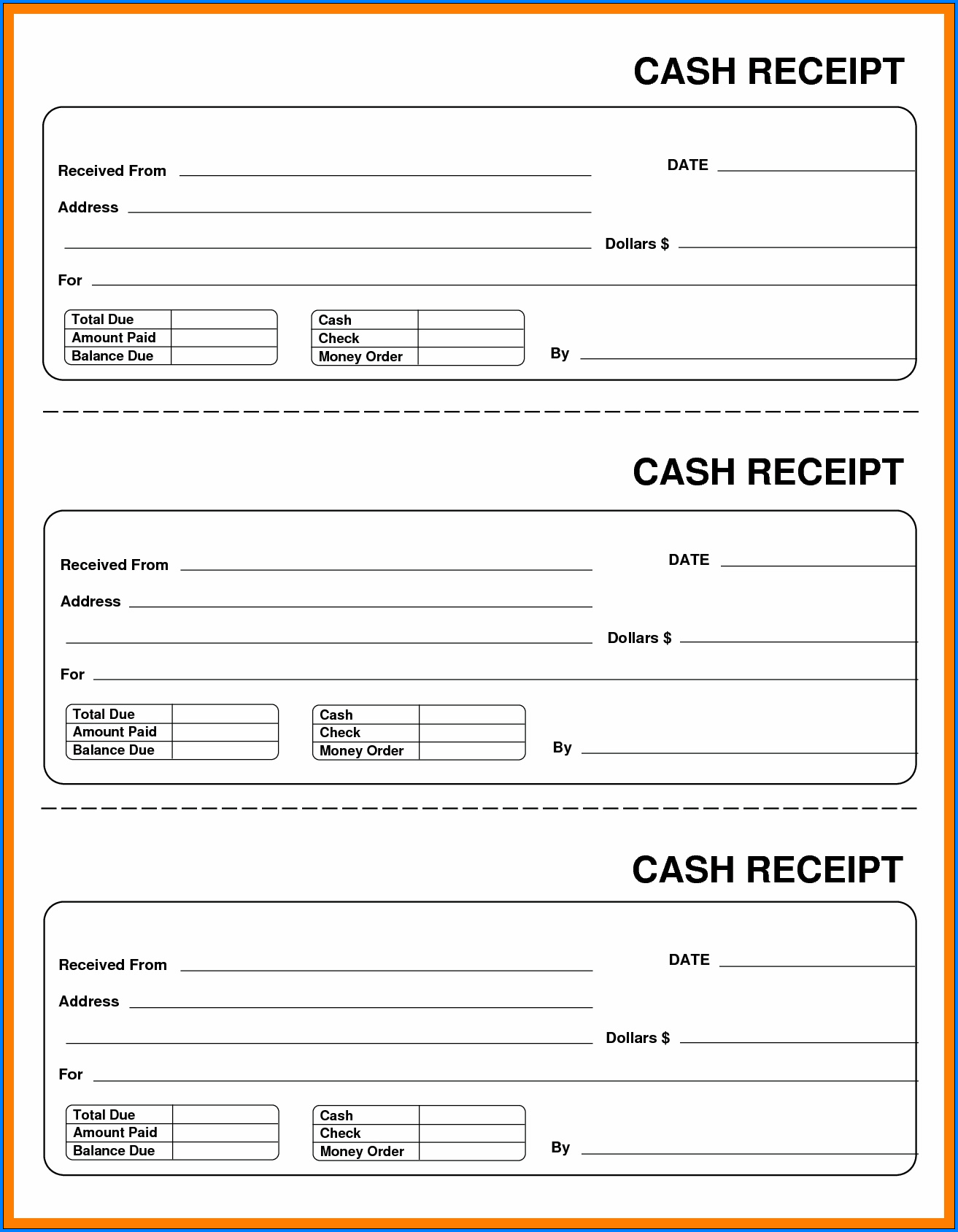

In some cases, you might receive a check or cash payment from a customer later on. In these cases, you will need to make a separate cash received journal entry to record this information. You must also track how these payments impact customer invoices and store credit. To make sure you have cash receipt accounting down pat, check out the cash received journal entry examples below. Recording cash receipts offsets the accounts receivable balance from the sale.

Our Team Will Connect You With a Vetted, Trusted Professional

The totals from all the amount columns (other than the other account column) are posted to the appropriate general ledger accounts. As these accounts are posted, the account number is entered into the post reference column. In the subsidiary ledger, the post reference is “CR-8”, which indicates that the entries came from page 8 of the cash receipts journal.

Record Retention for Businesses

The debit columns in a cash receipts journal will always include a cash column and, most likely, a sales discount column. Other debit columns may be used if the firm routinely engages in a particular transaction. This format in effect combines both two column formats discussed above in that it uses the additional columns to record both discounts and bank account transactions. As before the first three columns in the diagram are the date, transaction description (Desc.), and ledger folio reference (LF). The two columns referred to in the name of this cashbook are the monetary amount of the cash receipt (Cash), and the monetary amount of the receipts into the current bank account of the business (Bank), both highlighted in gray. For example, when a company purchases merchandise from a vendor, and then in turn sells the merchandise to a customer, the purchase is recorded in one journal and the sale is recorded in another.

Cash Receipt Journal – Definition, Explanation, Format, and More

This summary is ordinarily made in your business books (for example, accounting journals and ledgers). Your books must show your gross income, as well as your deductions and credits. The first three columns in the diagram are the date, transaction description (Desc.), and ledger folio reference (LF). The single column referred to in the name of this cash ledger book is the monetary amount of the cash receipt (Cash) highlighted in gray. Journal and Ledger are the two pillars which create the base for preparing final accounts. The Journal is a book where all the transactions are recorded immediately when they take place which is then classified and transferred into concerned account known as Ledger.

Get Your Questions Answered and Book a Free Call if Necessary

- Cost of sales is also known as the cost of goods sold, and the two terms are used interchangeably.

- Although these amounts are often posted at the end of the month, they could be posted more frequently.

- Manual accounting systems will likely use special journals for recording routine transactions.

- Provides a chronological record of all credit sales made in the life of a business.

The right hand, payments side (credit) would be identical in structure and format. To keep your books accurate, you need to have a cash receipts procedure in place. Your cash receipts process will help you organize your total cash receipts, avoid accounting errors, and ensure you record transactions correctly. The cash disbursement diary and the cash receipts journal are typically divided. In contrast to a cash account, which is an account within a general ledger, a cash receipts journal is a separate ledger.

Cash Basis Accounting is a type of accounting whereby all of the company’s revenues are recognised upon actual cash receipt and all of the expenses are recognised upon payment. Read on as we take a closer look at what a cash receipts journal is, the different types, and the pros and cons. If you accept checks, be sure to also include the check number with the sales receipt. To make sure your books are as accurate as possible, make sure you organize business receipts using a storage system (e.g., filing cabinets or computer). It also ensures that the business can keep track of all the account receivables and aged receivables.

Similarly, it also provides an easy way to keep track of all the unpaid supplier and vendor payments by allowing the business to quickly see what cash was received and paid out during a said period. In this case the debit entry to the cash account represents the cash collected from customers for the period, which increases the asset of cash. You must be able to substantiate certain elements of expenses to deduct them on your tax return. The Supreme Court has authority to appoint a successor signatory for the attorney trust account. Thelawyer must safeguard and segregate those assets from the lawyer’s personal,business or other assets. The other side of the cash book has the heading ‘Credit’ and shows an identical format with the single column representing the monetary amount of the cash payment.

Chronological entries are made in the how to calculate your accounts payable ap cost per invoice and the balance is continuously updated and confirmed. Since no cash is received from credit sales transactions, they are not recorded in an accounting journal. Credit sales are handled using the accrual basis of accounting, while cash transactions are handled using the cash basis. The credit sales which the busy ones make are not recorded in the cash journal as no cash is received while these sales transactions occur.